VAT

- Skip Ahead to

- Overview

- Adding your VAT number

- What to do if you forget to enter your VAT number

- Actions supported by the VAT initiative

- Benefits of the VAT initiative

- GST (Australia)

- Sales tax (United States)

- EU VAT

- EU VAT - Rates

- EU VAT - Exemptions

- EU VAT - Charities and nonprofit organizations

- EU VAT - Article 151 exemption

- Switzerland VAT

- Indonesia VAT

- Indonesia VAT – E-Invoicing/e-Faktur Pajak

- South Africa VAT

- Singapore GST

- New Zealand GST

- Norway VAT

- Iceland VAT

- South Korea VAT

- Canada GST/HST

- Canada QST

- Canada - British Columbia and Saskatchewan Provincial Sales Tax

Overview

Asana customers will be charged VAT or GST in certain jurisdictions as a result of legislation which requires overseas companies who provide digital services, such as Asana, to collect VAT or GST.

Certain jurisdictions do not require VAT or GST to be charged when customers are registered for VAT or GST purposes. Such customers should provide their VAT or GST registration numbers to Asana to ensure that they are not charged VAT or GST.

Please note that none of the information provided here should be considered tax advice, but a general overview of relevant tax rules and requirements. Please consult with your professional tax advisor for tax advice based on your specific facts and circumstances.

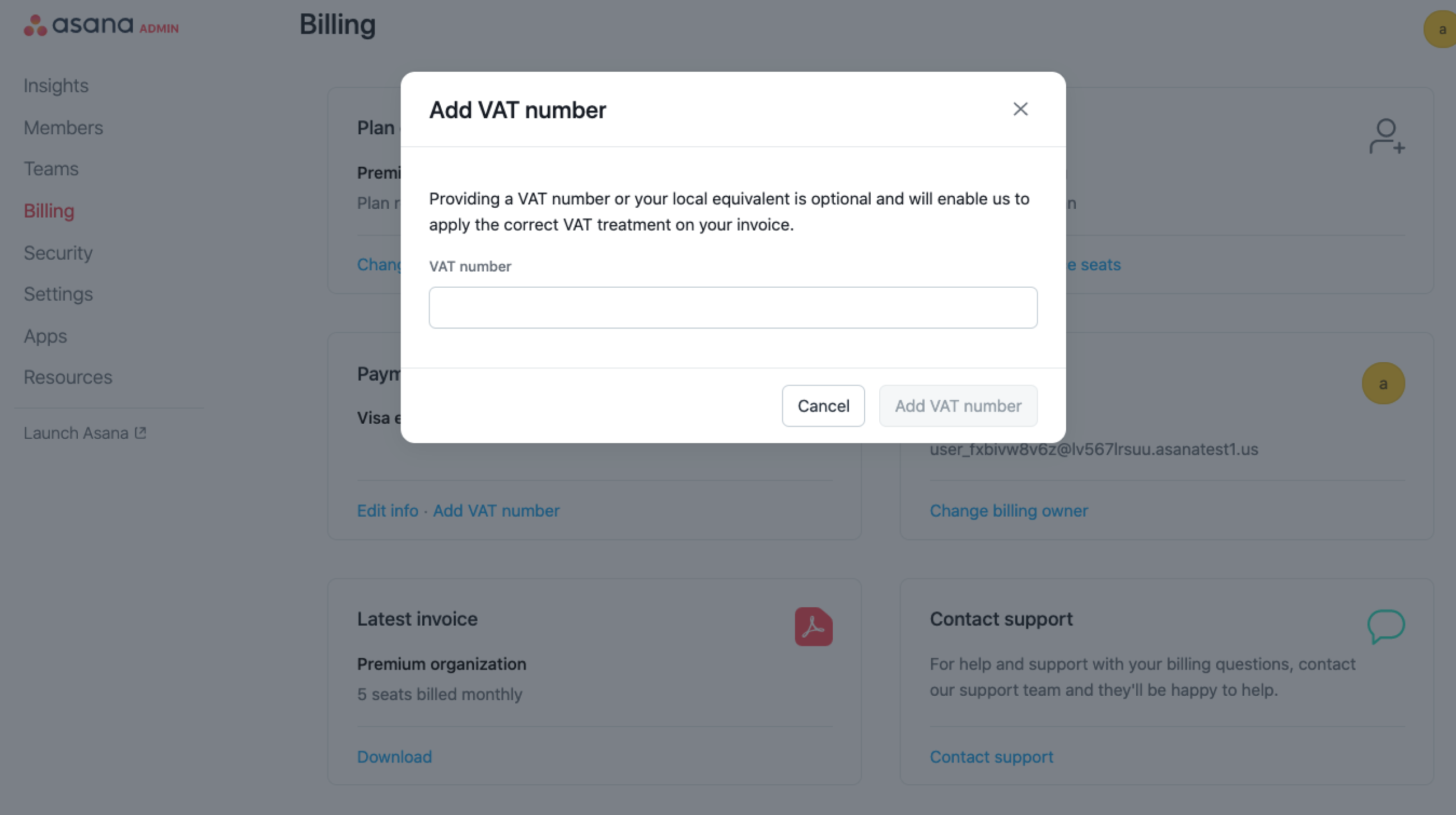

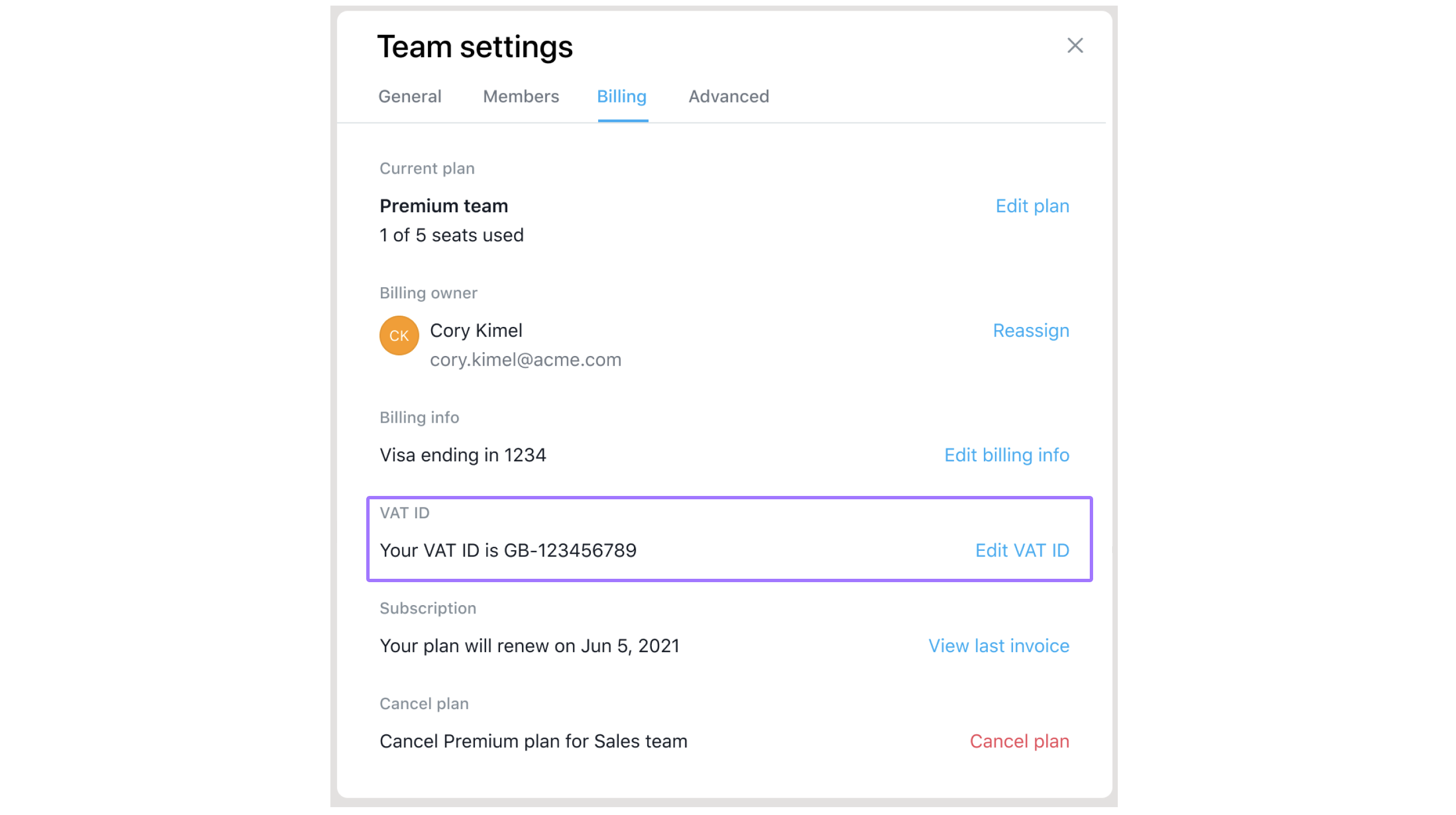

Adding your VAT number

To add your VAT ID:

- Navigate to the Admin console for paid organization and divisions, or Team settings for paid teams

- Click on the Billing tab

- Select Add VAT Number

Add VAT number through the billing tab of the admin console, available in paid organizations and divisions.

Add VAT number through the billing tab of team settings for paid teams.

What to do if you forget to enter your VAT number

You may add your VAT number at any time via the billing tab in the admin console or team settings. In doing so, future invoices will not include VAT.

In the event that you forget to enter your VAT number and have then been charged EU VAT, please contact Asana’s Support team for assistance.

Actions supported by the VAT initiative

Admin Console

You will now be able to add your VAT number to your account through the billing tab of the admin console for paid organizations and divisions, or the billing tab of the team settings for paid teams.

Direct contact with the Asana Support team

The update will allow for you to directly contact Asana’s Support team who will then be able to add the VAT ID to the Asana account on your behalf.

Direct contact for refunds

You will also have the ability to directly contact the Asana Support team in the event that you require a refund.

Benefits of the VAT feature

The VAT feature will allow for users outside of the EU to obtain VAT/GST exemptions. Different countries are eligible for different exemptions depending on their location and VAT/GST requirements.

Sales tax (United States)

Customers in the US may be subject to state and local sales and use taxes.

The “Sold To” address is used to determine whether your invoice is subject to tax. This information is subject to cross-referencing to ensure the address is accurate.

If you qualify for a tax exemption in the US, Asana users should submit their tax exemption documentation (such as an exemption certificate, resale certificate, or a direct-pay permit) to our Support team.

From here, the documentation will be reviewed and your account tax exemption status will be updated accordingly.

Please ensure that the tax exemption documentation corresponds with the US state listed in your “Sold To” address and that the entity name on the certificate matches the customer name in your customer profile.

GST (Australia)

Asana is registered as a non-resident vendor under the Simplified GST regime.

Asana is required to collect GST from all customers located in Australia unless they are registered for GST and provide an ABN (Australian Business Number). The “Sold To” address associated with the customer account will then be used to determine whether or not you are located in Australia.

If you are registered for GST in Australia and add your ABN (Australian Business Number) in the Admin Console, you will not have GST added to future invoices. You may, however, have obligations to report that purchase under the reverse-charge mechanism. Please consult with your tax advisors to determine what, if any, obligations may exist.

To add your VAT ID:

- Navigate to the Admin console for paid organization and divisions, or Team settings for paid teams

- Click on the Billing tab

- Select Add VAT Number

This information, including the “Sold To” address, will be subject to verification and validation.

EU VAT

EU VAT is charged based on the Sold To country address in your customer profile.

This includes all 27 Member States in the EU:

- Austria

- Belgium

- Bulgaria

- Croatia

- Cyprus

- Czech Republic

- Denmark

- Estonia

- Finland

- France (including Monaco for the purposes of VAT)

- Germany

- Greece

- Hungary

- Ireland

- Italy

- Latvia

- Lithuania

- Luxembourg

- Malta

- Netherlands

- Poland

- Portugal

- Romania

- Slovakia

- Slovenia

- Spain

- Sweden

EU VAT - Rates

Asana is registered under the Non-Union One Stop Shop “OSS”.

Under OSS, Asana will be required to charge VAT at the rate applicable to your location, unless a valid VIES VAT number intra-community VAT number/ID is provided.

The “Sold To” address associated with the customer account is then used to determine whether a customer is located in the EU, and if so, in which EU country.

VAT - Exemptions

Once confirmed in the VIES database, if you provide a valid VAT number you will not be charged VAT. You may, however, have obligations to report the purchase under the reverse-charge mechanism.

EU VAT - Charities and nonprofit organizations

Generally, most charities will not be registered for EU VAT purposes as they do not have business operations. As such, if the organization is not registered, VAT may still be charged on purchases from Asana.

EU VAT - Article 151 exemption

The EU VAT Directive provides an exemption to certain international and diplomatic bodies under Article 151 of the directive.

If you qualify for the exemption, you will be issued written documentation indicating tax exempt status from the tax authority in the EU member state within which you are registered for VAT. It is necessary that you forward this documentation to Asana’s Support team for review.

Alternatively, you may be eligible for a VAT refund directly from your local tax authority.

Switzerland VAT

The Swiss Federal Tax Administration requires that companies domiciled in Switzerland or that provide supplies of goods or services to customers in Switzerland become liable for VAT. This requirement also applies to companies based abroad. Further information on non-resident VAT registration requirements in Switzerland may be obtained here. As such, Asana collects Swiss VAT at the prevailing rates on supplies to all customers (B2C and B2B) located in Switzerland.

Due to Asana’s VAT registration in Switzerland and the legal agreement between Switzerland and the Principality of Liechtenstein pertaining to the integration of Swiss VAT law into its own state law, Asana is required to collect VAT from customers in Liechtenstein as well.

The “Sold To” address associated with the customer account will then be used to determine whether or not you are located in Switzerland or Liechtenstein for VAT purposes.

Indonesia VAT

Non-resident suppliers of intangible goods and/or services through an e-commerce system are required to charge VAT on their supplies to Indonesian customers. Asana has been appointed as a VAT collector by Director General of Tax (DGT) in Indonesia. Asana collects Indonesian VAT at the prevailing rates on supplies to all customers (B2C and B2B) located in Indonesia.

The “Sold To” address associated with the customer account will then be used to determine whether or not you are located in Indonesia for VAT purposes. This information is cross-referenced to ensure the address is accurate.

Indonesia VAT – E-Invoicing/e-Faktur Pajak

Asana, as a non-resident provider, is not required to provide an electronic invoice. Instead, Asana provides a VAT receipt in the form of an invoice which may be used to substantiate input VAT credit claims. Please ensure you provide Asana with your valid tax identification number (15 digits in length), full registered name and email address (optional).

Please refer to Adding your VAT Number for help on how to add your tax identification number in order for it to appear on your invoice.

South Africa VAT

Non-resident suppliers of electronically supplied services are required to charge VAT on their supplies to South African customers. Asana is registered as a VAT vendor in South Africa. As such, Asana collects South African VAT at the prevailing rates on its electronically supplied services to all customers (B2C and B2B) located in South Africa.

The “Sold To” address associated with the customer account will then be used to determine whether or not you are located in South Africa for VAT purposes. This information is cross-referenced to ensure the address is accurate and the customer is considered to be located in South Africa for VAT purposes.

Singapore GST

Non-resident suppliers of electronically supplied services (ESS) are required to register and collect GST on ESS supplies made to customers in Singapore that are not registered for Singapore GST purposes (i.e., B2C supplies only).

If a customer provides its valid Singapore GST registration number to Asana, Asana will not charge Singapore GST as this supply will be considered a B2B supply. If you are not registered for Singapore GST, but are located in Singapore, Asana will be required to charge Singapore GST on its services to you.

The “Sold To” address associated with the customer account will then be used to determine whether or not you are located in Singapore for GST purposes.

B2B customers may have an obligation to self-report the GST under the reverse charge mechanism.

New Zealand GST

Non-resident suppliers of electronically supplied services (ESS) are required to register and collect GST on ESS supplies made to customers in New Zealand that are not registered for New Zealand GST purposes (i.e., B2C supplies only).

If a customer provides its valid New Zealand GST registration number or New Zealand business number to Asana, Asana will not charge New Zealand GST as this supply will be considered a B2B supply. If you are not registered for New Zealand GST, but are located in New Zealand, Asana will be required to charge New Zealand GST on its services to you.

The “Sold To” address associated with the customer account will then be used to determine whether or not you are located in New Zealand for GST purposes. This information is cross-referenced to ensure the address is accurate.

B2B customers may have an obligation to self-report the GST under the reverse charge mechanism.

Norway VAT

Non-resident suppliers of electronically supplied services (ESS) are required to register and collect VAT on ESS supplies made to customers in Norway that are not registered for Norwegian VAT purposes (i.e., B2C supplies only).

If a customer provides its valid Norwegian VAT identification number to Asana, Asana will not charge Norwegian VAT as this supply will be considered a B2B supply. If you are not registered for VAT in Norway, but are located in Norway, Asana will be required to charge VAT on its services to you.

The “Sold To” address associated with the customer account will then be used to determine whether or not you are located in Norway for VAT purposes. This information is cross-referenced to ensure the address is accurate.

B2B customers may have an obligation to self-report the VAT under the reverse charge mechanism.

Iceland VAT

Non-resident suppliers of electronically supplied services (ESS) are required to register and collect VAT on ESS supplies made to customers in Iceland that are not registered for Icelandic VAT purposes (i.e., B2C supplies only).

If a customer provides its valid Icelandic VAT identification number to Asana, Asana will not charge Icelandic VAT as this supply will be considered a B2B supply. If you are not registered for VAT in Iceland, but are located in Iceland, Asana will be required to charge VAT on its services to you.

The “Sold To” address associated with the customer account will then be used to determine whether or not you are located in Iceland for VAT purposes. This information is cross-referenced to ensure the address is accurate.

B2B customers may have an obligation to self-report the VAT under the reverse charge mechanism.

South Korea VAT

Non-resident suppliers of electronically supplied services (ESS) are required to register and collect VAT on ESS supplies made to customers in Iceland that are not registered for South Korean VAT purposes (i.e., B2C supplies only).

If a customer provides its valid South Korean Business Registration Number to Asana, Asana will not charge South Korean VAT as this supply will be considered a B2B supply. If you are not registered for VAT in South Korea, but are located in South Korea, Asana will be required to charge VAT on its services to you.

The “Sold To” address associated with the customer account will then be used to determine whether or not you are located in South Korea for VAT purposes. This information is cross-referenced to ensure the address is accurate.

B2B customers may have an obligation to self-report the VAT under the reverse charge mechanism.

Canada GST/HST

Non-resident suppliers of certain specified supplies, such as software licenses, are required to charge Canadian GST/HST on their supplies to Canadian customers who are not registered for GST/HST purposes.

If a customer provides its valid GST/HST number to Asana, Asana will not charge GST/HST. If you are not registered for GST/HST in Canada, but are located in Canada, Asana will be required to charge GST/HST on its services to you.

The “Sold To” address associated with the customer account will then be used to determine whether or not you are located in Canada for GST purposes, and if so, what GST/HST rate is applicable. This information is cross-referenced to ensure the address is accurate.

Certain customers may have an obligation to self-report the GST/HST under the reverse charge mechanism.

Canada QST

Non-resident suppliers of certain specified supplies, such as software licenses, are required to charge Quebec Sales Tax (QST) on their supplies to Quebec customers who are not registered for QST purposes.

If a customer provides its valid QST number to Asana, Asana will not charge QST. If you are not registered for QST purposes, but are located in Quebec, Asana will be required to charge QST on its services to you.

The “Sold To” address associated with the customer account will then be used to determine whether or not you are located in Quebec for QST purposes. This information is cross-referenced to ensure the address is accurate.

Certain customers may have an obligation to self-report the QST under the reverse charge mechanism.

Canada - British Columbia and Saskatchewan Provincial Sales Tax

Non-resident suppliers of certain services, such as software licenses, are required to charge provincial sales tax (PST) on their supplies to customers based in either British Columbia or Saskatchewan.

The “Sold To” address associated with the customer account will then be used to determine whether or not you are located in British Columbia or Saskatchewan for PST purposes. This information is cross-referenced to ensure the address is accurate.

Some limited PST exemptions may be available to customers (e.g., purchases for resale). Please contact our Customer Service team with your documentation to have the exemption reviewed and processed.